5 Private Capital Insights from Q4 2024 and What They Mean to You

November 22, 2024

As we near the end of 2024, the latest edition of our Private Capital industry report provides actionable insights from the industry designed to keep investors and business owners informed on current trends impacting private equity, private credit, and private real estate.

If you would like to discuss how private investments fit into your portfolio, please reach out to your Aprio advisor, Simeon Wallis, CFA, Partner and Chief Investment Officer, or Adam Niestradt, CFA, Director of Private Capital.

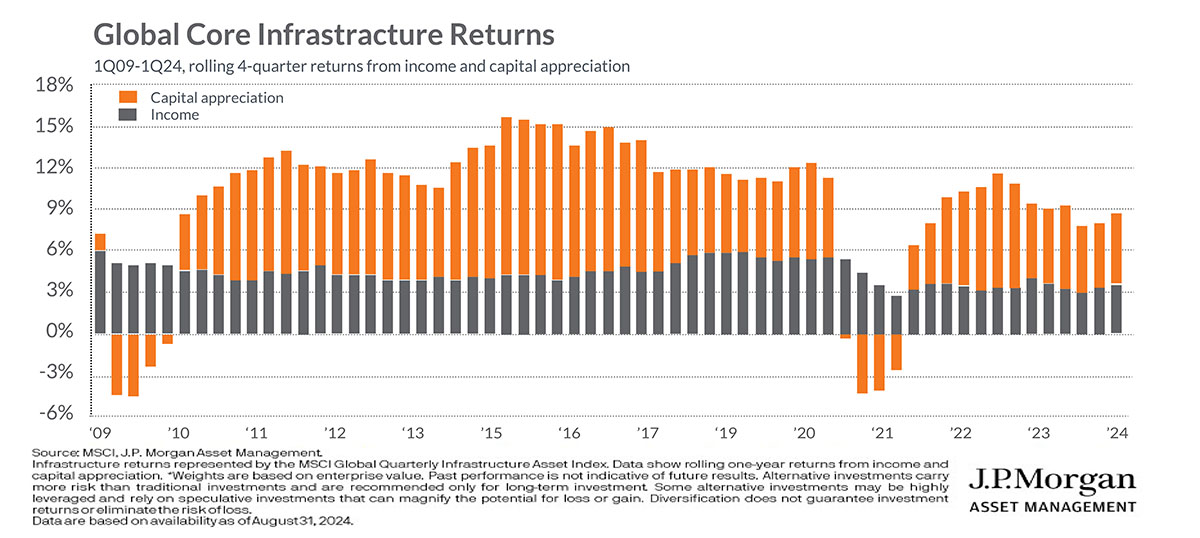

1. Infrastructure can provide stable returns and income

Global core infrastructure returns from Q1 2009 to Q1 2024 reveal a clear pattern: income returns remained stable throughout, while capital appreciation experienced notable volatility. Key periods of fluctuation occurred between 2012-2015 and during the pandemic in 2020-2021. This consistency in income highlights the sector’s resilience, while the variability in capital appreciation underscores its sensitivity to broader economic events.

What it Means for You: Infrastructure investments are proving to be resilient, especially when it comes to generating stable income returns. Income from infrastructure assets has remained consistent even during volatile periods like the global financial crisis and the COVID-19 pandemic, making this asset class an attractive option for investors looking for stable yields. The fluctuations in capital appreciation, particularly the dip during the 2020 pandemic, underscore the sensitivity of asset valuations to macroeconomic shocks. This means that for investors, infrastructure can serve as a reliable income source, while its appreciation potential might be more cyclical. Business owners in infrastructure-related industries, such as power and transportation, can anticipate robust investor interest, particularly for projects that promise stable cash flows.

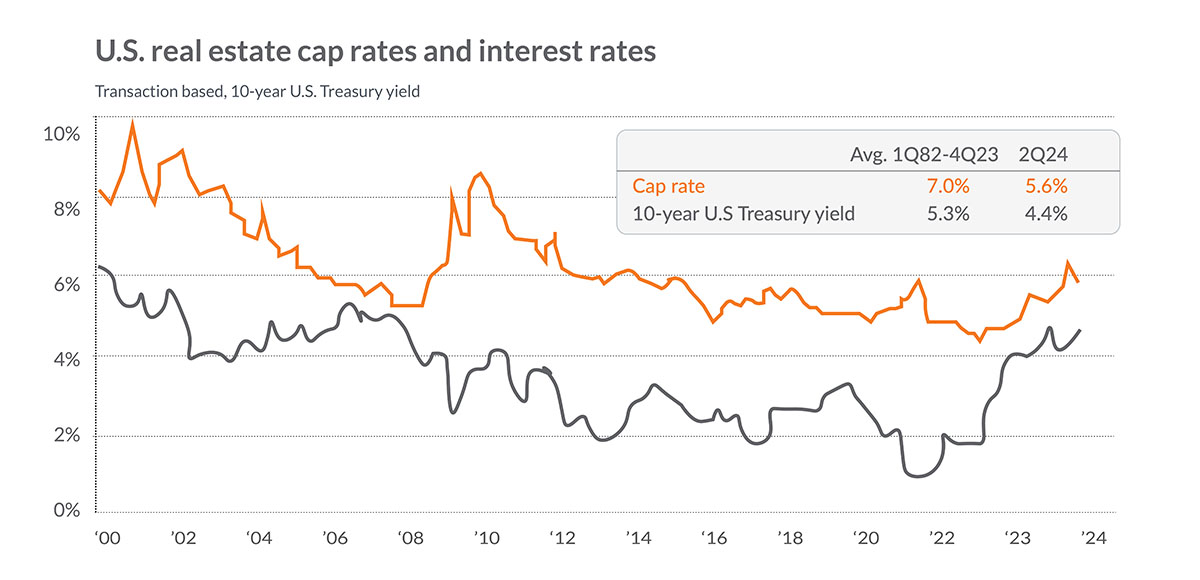

2. Real estate returns, cap rates, and interest rate connections

U.S. real estate cap rates, representing expected returns on real estate investments, and the 10-year U.S. Treasury yield, reflecting the risk-free rate of return, display distinct trends from 2000 to Q2 2024. Cap rates show a steady decline from the early 2000s to around 2015, followed by periods of fluctuation and a recent upward trend. The data also reveals a clear relationship between cap rates and Treasury yields, with cap rates generally aligning with movements in broader interest rates. This highlights how shifts in the risk-free rate influence real estate return expectations over time.

What it Means for You: Cap rates and Treasury yields have a direct influence on real estate valuations. When Treasury yields are low, as seen around 2012 to 2014 and 2020 to 2021, real estate cap rates also declined, making property values relatively more expensive as investors sought higher yields amid low bond returns. The recent uptick in both cap rates and Treasury yields indicates a repricing of risk, with real estate yields becoming more competitive. For investors, this means a shift towards a more balanced yield environment, where real estate assets may become less expensive compared to the high-demand, low-yield era of 2020 to 2021. For real estate owners, understanding the rising cap rates will be essential for pricing expectations in upcoming transactions, as higher cap rates imply a downward pressure on property valuations. This is a good time for investors to closely evaluate market entry points, particularly as higher cap rates might provide a more favorable return on investment given the current interest rate environment.

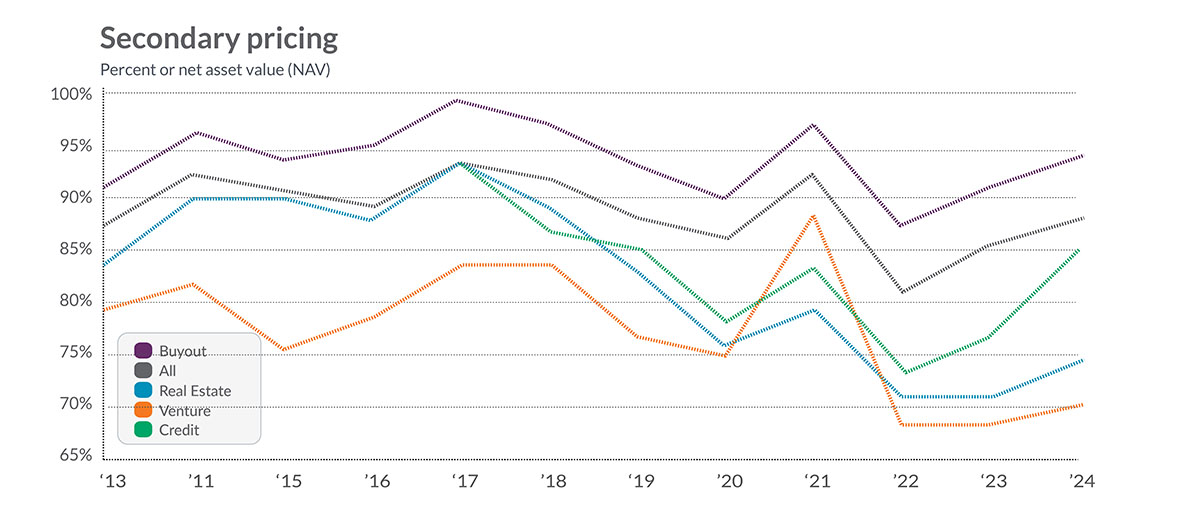

3. Secondary pricing has rebounded, but still provides value

The purchasing of existing investments in private capital funds, a.k.a. “secondaries,” has grown significantly in the last decade. Secondary pricing as a percentage of Net Asset Value (NAV) across private market asset classes from 2013 to 2024 reveals important trends. Buyout funds consistently command the highest pricing, reaching 94% of NAV in 2024, reflecting their strong market appeal. Credit funds, in contrast, display significant variability, rebounding to 85% in 2024 after a sharp decline during 2020-2021. These patterns underscore the resilience of buyout funds and the sensitivity of credit funds to economic disruptions, highlighting differing risk and return dynamics across asset classes.

What it Means for You: The secondary market has shown resilience, particularly in buyout and real estate segments. The high pricing of buyouts (at 94% of NAV) reflects strong demand for high-quality buyout funds, likely driven by their established performance track record and lower perceived risk. The variance observed, especially in credit and venture segments, highlights greater risk and the challenges these asset classes face during uncertain economic periods. For investors, this suggests that while buyout funds on the secondary market can provide attractive opportunities for lower discounts, sectors like venture and credit might offer value, especially when discounts are higher. This can be a tactical entry point into otherwise inaccessible funds. Business owners looking to raise secondary capital should focus on ensuring their assets remain attractive by maintaining strong performance, as this will support higher secondary pricing in potential liquidity events.

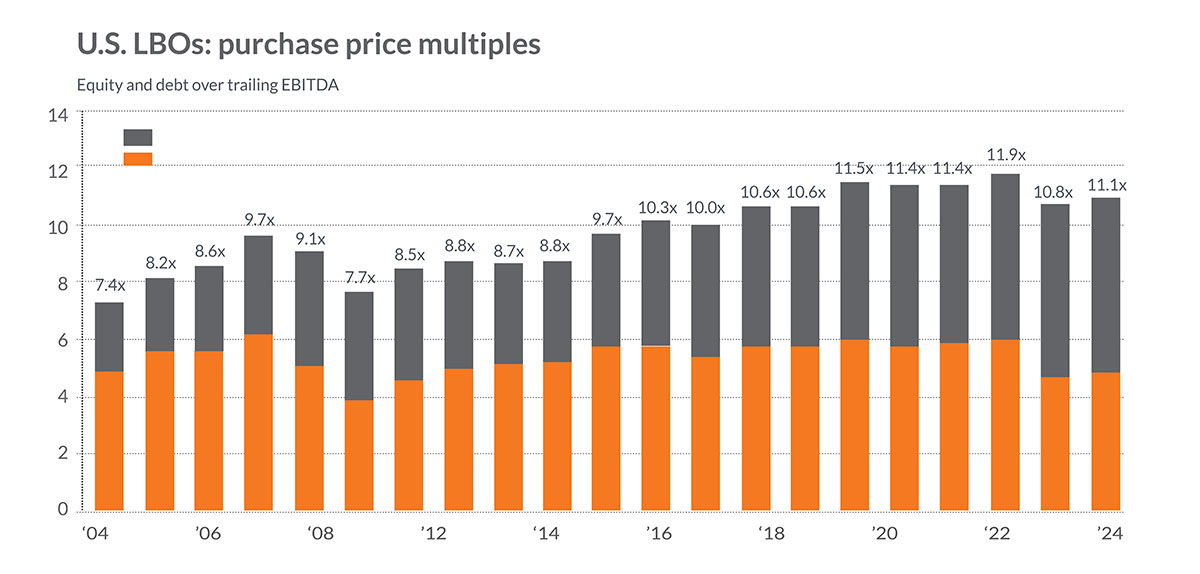

4. Private equity multiples have come down

Although slightly higher than 2023, total purchase multiples in private equity have come down following their post-COVID high. Notably, leverage has decreased in lower debt multiples as shown in the chart above (in blue). This means private equity funds are relying less on debt and putting more equity into their deals.

What this means for you: This chart highlights the rising costs of acquiring companies in the U.S. LBO market, driven by high valuations and competitive deal-making environments. The recent decline in purchase price multiples suggests a more cautious approach by buyers, potentially in response to economic uncertainties and higher interest rates affecting financing costs. For private equity investors, this means that future returns might rely more heavily on operational improvements within portfolio companies rather than financial engineering through high leverage. It’s essential to partner with managers who can create value post-acquisition, especially as reliance on debt for LBOs becomes more constrained by the economic environment.

5. Private credit can help stabilize portfolios during periods of stress

The market value (as a percentage of par) of broadly syndicated loans and private equity-backed private loans from Q3 2018 to Q4 2023 highlights three critical periods of market impact.

- Q4 2018 to Q1 2019 – Market values declined due to uncertainties surrounding U.S.-China trade tensions and Brexit.

- Q1 2020 to Q3 2021 – A sharp drop, particularly in broadly syndicated loans, as the COVID-19 pandemic disrupted global supply chains and economic stability. Private equity-backed loans rebounded more quickly, recovering closer to their original value by Q3 2021.

- Q1 2022 to Q4 2023 – Persistent global conflicts (notably involving Russia and China) and rising inflation drove both loan types lower. Although both showed signs of gradual recovery toward the end of 2023, private equity-backed loans maintained a slight premium over broadly syndicated loans.

What this means for you: This chart underscores the resilience and relative stability of private equity-backed loans compared to broadly syndicated loans during periods of economic uncertainty. For private credit investors, this resilience suggests that private equity-backed loans may provide a more stable income stream in volatile markets. However, it’s crucial to recognize the ongoing risks associated with inflation and geopolitical tensions, which can affect loan valuations. Allocating to private credit managers with experience in high-quality, private equity-backed loans could enhance portfolio stability and offer better downside protection in uncertain environments.

Disclosure:

Investment advisory services are offered by Aprio Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisor. Opinions expressed are as of the publication date and subject to change without notice. Aprio Wealth Management, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary is for informational purposes only and has not been tailored to suit any individual. References to specific securities or investment options should not be considered an offer to purchase or sell that specific investment.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. No graph, chart, or formula in this presentation can be used in and of itself to determine which securities to buy or sell, when to buy or sell securities, whether to invest using this investment strategy, or whether to engage Aprio Wealth Management, LLC’s investment advisory services.

Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. Any securities mentioned in this commentary are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. Before making any investment decision, investors should read and consider all the relevant investment product information. Investors should seriously consider if the investment is suitable for them by referencing their own financial position, investment objectives, and risk profile before making any investment decision. There can be no assurance that any financial strategy will be successful.

Certain investor qualifications may apply. Definitions for Qualified Purchaser, Qualified Client and Accredited Investor can be found from multiple sources online or in the SEC’s glossary found here https://www.sec.gov/education/glossary/jargon-z#Q.

Recent Articles

About the Author

Simeon Wallis

Simeon Wallis, CFA, is a Partner, the Chief Investment Officer of Aprio Wealth Management, and the Director of Aprio Family Office. Each month, Simeon brings you insights from the financial markets in Aprio’s Pulse on the Economy. To discuss these ideas and how they may affect your current investment strategy, schedule a consultation.

Adam Niestradt

Adam Niestradt, CFA is the Director of Private Capital at Aprio Wealth Management. Adam has over a decade of investment experience with high and ultra-high net worth families with a focus on private capital investments. To discuss these ideas and how they may affect your current investment strategy, email Adam directly at adam.niestradt@aprio.com

Stay informed with Aprio.

Get industry news and leading insights delivered straight to your inbox.