6 Manufacturing & Distribution Insights from Q4 2024 and What They Mean for You

November 8, 2024

While the U.S. manufacturing & distribution sectors remain challenged, there are signs of bottoming out.

The U.S. manufacturing sector continues to contract, with the PMI declining to 46.5, its lowest reading this year. While the U.S. manufacturing sector remains under pressure, New Orders and Employment declined at slower rates than prior months. Meanwhile, a rebalancing labor market is easing wage pressures. Perhaps most significantly, manufacturing and distribution companies that are maintaining stable margins focus intensely on operational efficiency and strategic cost control, particularly in response to persistent transportation and logistics challenges.

We delve into each of these developments below, providing a closer inspection of what they might mean for you and your organization in the coming months.

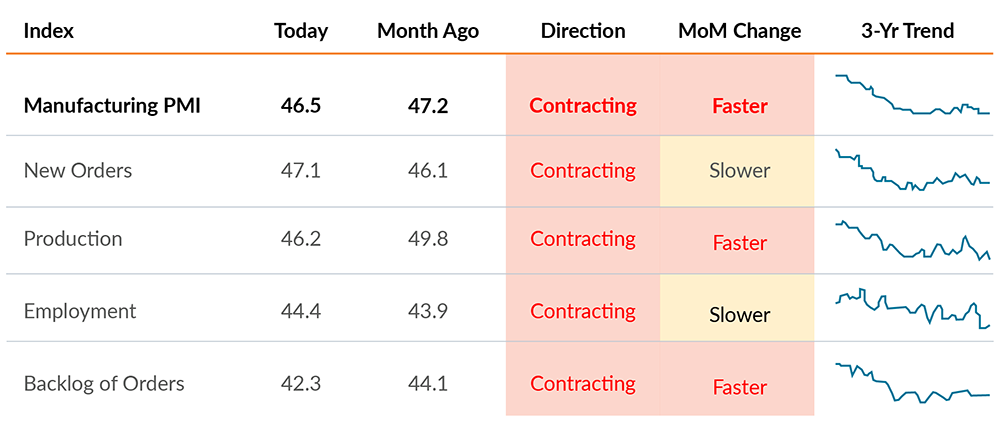

1. PMI stagnates in contraction territory, with employment falling faster.

ISM Snapshot

Source: Institute of Supply Management (ISM)

The Manufacturing PMI declined to 46.5, indicating continued contraction within the U.S. manufacturing sector. It has been below 50 in 23 of the last 24 months. New Orders slightly improved to 47.1, up from 46.1 last month. Meanwhile, Production dropped to 46.2, reversing the prior month’s gains. With these metrics remaining below 50, surveys clearly highlight ongoing challenges in demand and output. The Backlog of Orders also retreated, declining to 42.3, suggesting weakened future production. There was a bright spot in Employment, which rose to 44.4.

What this means for you:

Demand and production level headwinds continue.

Manufacturers should focus on managing production and labor capacities efficiently, while also staying nimble to fluctuating orders and backlogs. Careful inventory and labor management will be key to sustaining profitability.

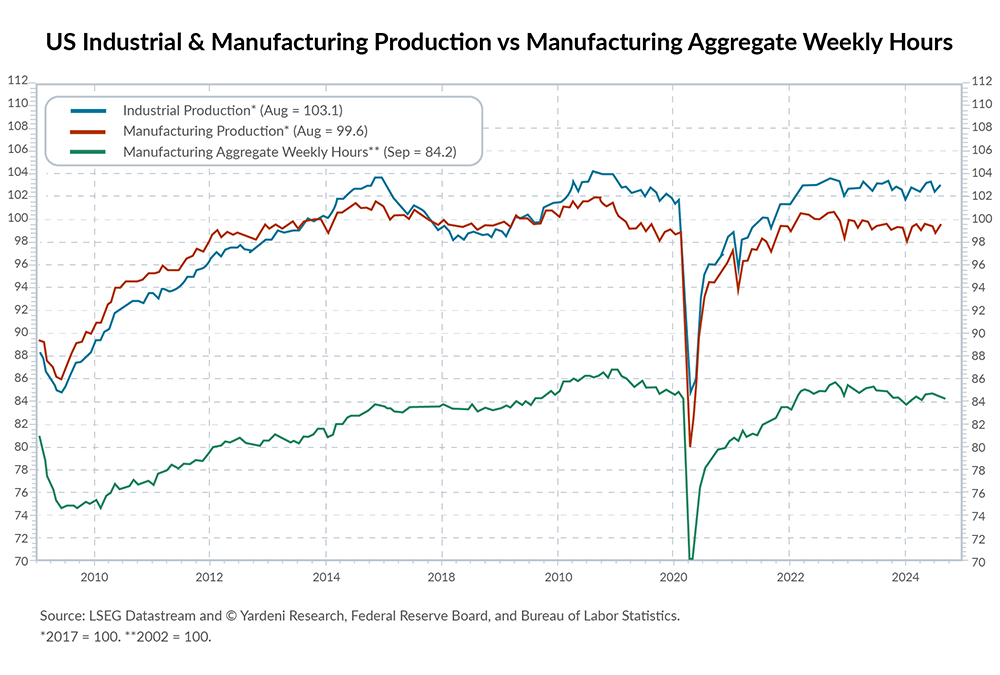

2. Production stabilizes, but recovery remains slow and uneven.

Industrial Production

Source: Yardeni Research

U.S. industrial production and manufacturing output showed slight signs of stabilization. Industrial production has recovered marginally, though it remains below pre-pandemic levels. Moreover, manufacturing aggregate weekly hours began to stabilize, suggesting that businesses are adjusting their labor utilization in line with current production needs. But while the data shows some recovery, growth is not robust and output remains subdued, compared to earlier peaks in 2022 and 2023.

What this means for you:

The stabilization in production and hours worked can be seen as a sign of cautious optimism. However, the slow recovery indicates that businesses remain conservative in their growth projections.

Efficiency improvements in labor utilization will be essential as manufacturers look to balance production with fluctuating demand. Additionally, when managing supply chains, muted industrial output means planning for longer timelines, given the modest pace of recovery.

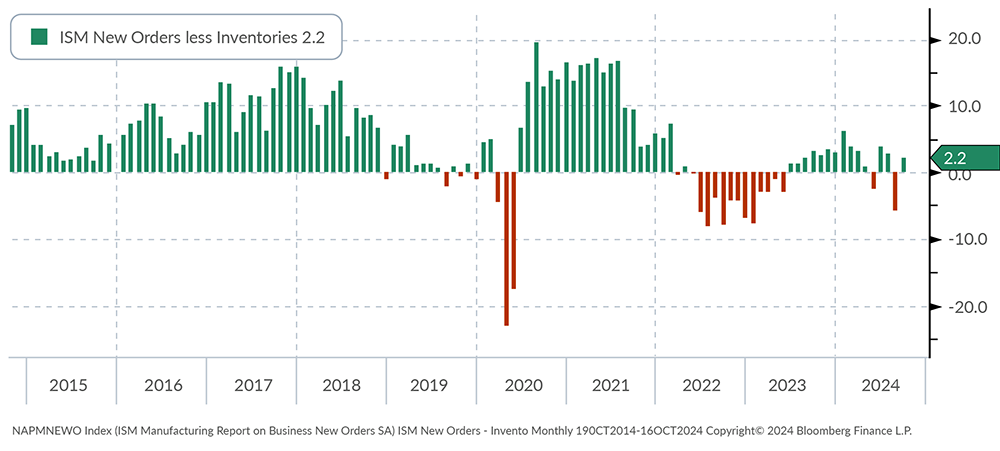

3. Inventories are being managed cautiously while new orders contract slower.

ISM New Orders less Inventories

Source: Bloomberg Finance, LP

New orders for manufactured goods have experienced a slight increase relative to inventory levels, according to the ISM New Orders less Inventories index. This indicates a more balanced relationship between incoming orders and inventory management, with new orders growing at a moderate pace compared to Q3. However, growth is still subdued, and businesses are cautious about investing in excess inventory, reflecting ongoing uncertainties in demand.

What this means for you:

The careful balance between new orders and inventory levels is a signal that supply chains have mostly healed from the pandemic challenges.

Managing inventory efficiently is critical while demand remains modest. Businesses should focus on adjusting forecasts frequently and aligning production schedules to avoid potential overstock or shortages, both of which could impact profitability and operational efficiency.

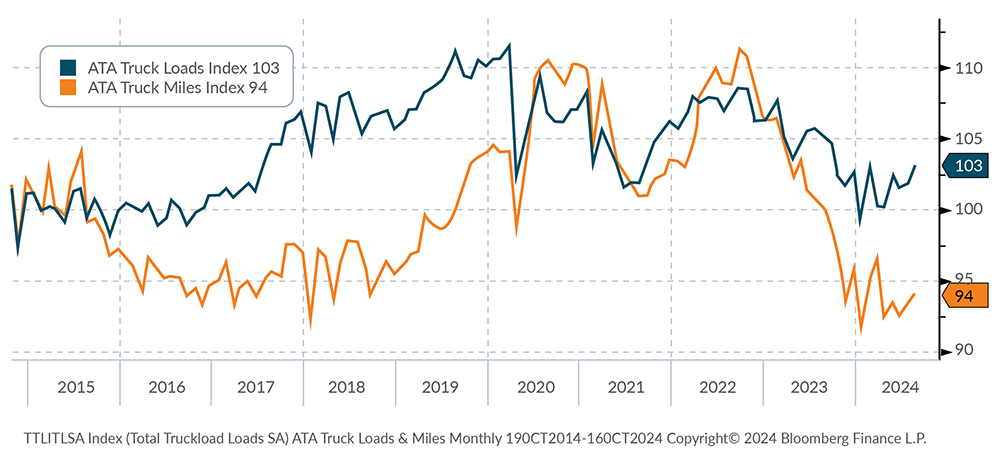

4. Shorter distribution routes drive higher truck loads but fewer miles.

ATA Truck Loads & Miles

Source: Bloomberg Finance, LP

Transportation metrics have shown a divergence between increasing truck loads and declining truck miles, according to the latest American Trucking Association (ATA) data. Truck loads have risen as manufacturers move more goods, but truck miles have decreased, indicating a shift toward shorter, more localized distribution routes. This trend may be driven by manufacturers seeking to minimize transportation costs and mitigate supply chain risks by sourcing and distributing closer to home.

What this means for you:

Manufacturers should take note of the changing logistics landscape.

With truck miles declining, focusing on regional supply chains could provide cost savings and improve delivery timelines. This shift also suggests an opportunity to optimize distribution strategies by partnering with local suppliers and reducing reliance on long-haul shipping. By shortening transportation distances, manufacturers can be more responsive to changes in customer demand, reduce delays, and improve overall supply chain resilience.

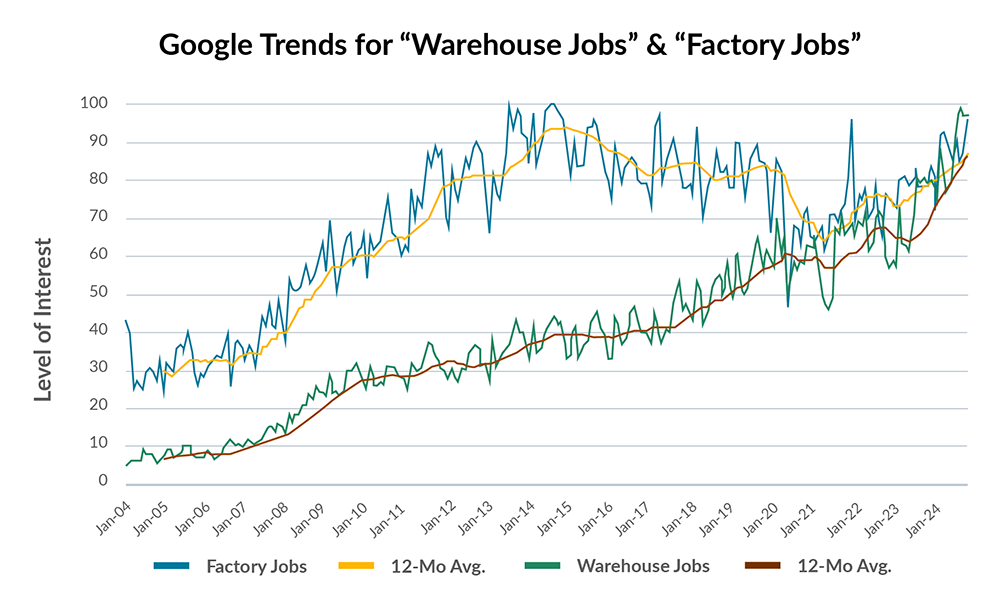

5. Rising interest in warehouse jobs contrasts with shrinking factory employment.

Google Trends for “warehouse jobs” & “factory jobs”

Source: Google Trends

Google Trends data highlights a significant rise in searches for “warehouse jobs” and “factory jobs,” reflecting heightened interest in employment within the manufacturing and distribution sectors. Despite the manufacturing sector contracting, the demand for factory jobs remains strong. In a similar vein, interest in warehouse jobs reflects the rising demand associated with growing logistics and distribution needs driven by several trends, including ecommerce and nearshoring/onshoring. The increased interest suggests that the labor market is becoming more balanced.

What this means for you:

For employers, the balanced labor market provides more options and flexibility when it comes to meeting staffing needs.

Furthermore, it reduces wage inflation pressures, which while not declining, the rate of year-over-year growth is slowing down.

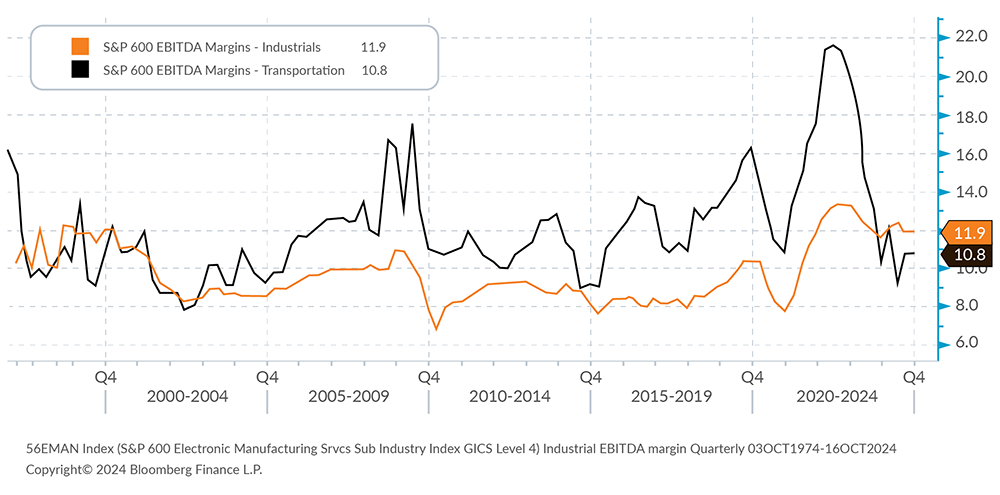

6. Stable margins for industrials, but transportation faces growing cost pressures.

EBITDA Margins

Source: Bloomberg Finance, LP

Manufacturers’ EBITDA margin trends differed across sectors. S&P 600 data reveals that industrials have managed to maintain relatively stable margins, benefitting from better cost controls and a steady demand environment. In contrast, the transportation sector has faced margin pressures due to labor costs, insurance, and logistical challenges. These issues have increased operational expenses, putting pressure on profitability for businesses heavily reliant on transportation.

What this means for you:

Stable margins may mitigate economic challenges, but maintaining this stability requires a continued focus on operational efficiency and input costs.

Companies facing these headwinds may need to consider operational improvements by deploying management systems such as lean, strategic combinations (i.e., mergers) to reduce redundancies and supplier rationalization. Navigating these pressures will be critical to protect their bottom line in a challenging economic environment.

This commentary is brought to you by our advisors at Aprio. Have any questions? Don’t hesitate to contact our team today.

Disclosures

Investment advisory services are offered by Aprio Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisor. Opinions expressed are as of the publication date and subject to change without notice. Aprio Wealth Management, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary is for informational purposes only and has not been tailored to suit any individual. References to specific securities or investment options should not be considered an offer to purchase or sell that specific investment.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. No graph, chart, or formula in this presentation can be used in and of itself to determine which securities to buy or sell, when to buy or sell securities, whether to invest using this investment strategy, or whether to engage Aprio Wealth Management, LLC’s investment advisory services.

Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. Any securities mentioned in this commentary are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. Before making any investment decision, investors should read and consider all the relevant investment product information. Investors should seriously consider if the investment is suitable for them by referencing their own financial position, investment objectives, and risk profile before making any investment decision. There can be no assurance that any financial strategy will be successful.

Securities offered through Purshe Kaplan Sterling Investments, Member FINRA/SIPC. Headquartered at 80 State Street, Albany, NY 12207. Purshe Kaplan Sterling Investments and Aprio Wealth Management, LLC are not affiliated companies.

Certain investor qualifications may apply. Definitions for Qualified Purchaser, Qualified Client and Accredited Investor can be found from multiple sources online or in the SEC’s glossary found here https://www.sec.gov/education/glossary/jargon-z#Q

Recent Articles

About the Author

Simeon Wallis

Simeon Wallis, CFA, is a Partner, the Chief Investment Officer of Aprio Wealth Management, and the Director of Aprio Family Office. Each month, Simeon brings you insights from the financial markets in Aprio’s Pulse on the Economy. To discuss these ideas and how they may affect your current investment strategy, schedule a consultation.

Adam Beckerman, CPA, CGMA

Adam Beckerman is Aprio’s Manufacturing and Distribution Leader and Assurance Partner. Adam's team of 30 professionals focus on the manufacturing industry with 20+ years of experience enabling the success of manufacturing start-ups, growth companies and businesses preparing for equity events.

Stay informed with Aprio.

Get industry news and leading insights delivered straight to your inbox.